If a mortgage offer feels too perfect, too urgent, or too vague, pause before you send documents. A real mortgage path should give you a way to verify the company, understand who is contacting you, and compare official loan terms before you commit.

The safest move is simple: identify the company, verify the license, compare the Loan Estimate, and keep control of your information.

Key Takeaways

- Verify the company or mortgage professional through NMLS Consumer Access before sharing sensitive documents.

- A real Loan Estimate helps you compare interest rate, APR, closing costs, cash to close, and loan features.

- The CFPB says lenders must provide a Loan Estimate within three business days after receiving a mortgage application.

- Upfront-fee pressure, wire-only payment requests, deed-transfer language, and "stop talking to your lender" advice are serious red flags.

- If a quote came through Ratespedia or a partner, confirm the company name, role, licensing, and next step before uploading documents.

The short answer: verify before you trust the quote

A low mortgage rate is not automatically a scam. Lenders price loans differently, and brokers may be able to show options from several lending sources. The problem starts when the offer asks you to move faster than the details allow.

Before you share a Social Security number, upload income documents, or pay any fee, you should know who is asking, which company they represent, how they are licensed, and what the next official mortgage document will be.

Use this article as a checkpoint. It is not meant to make you suspicious of every offer. It is meant to help you separate a legitimate mortgage conversation from a risky one.

9 checks before you apply or upload documents

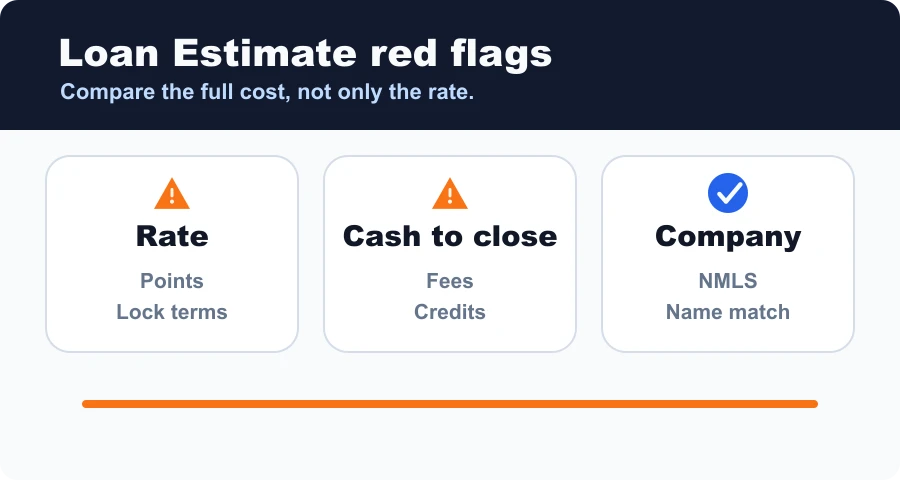

What a legitimate Loan Estimate should help you compare

The Consumer Financial Protection Bureau describes the Loan Estimate as a three-page form you receive after applying for a mortgage. It includes important loan details such as the estimated interest rate, monthly payment, total closing costs, taxes and insurance estimates, and special loan features.

The timing matters. The CFPB says the lender must provide a Loan Estimate within three business days after receiving your mortgage application.

3 business days

APR + costs

When you receive more than one offer, compare the same categories across each Loan Estimate. A lower rate with higher points or fees may not be cheaper. A lower monthly payment may hide a longer term, larger balloon risk, mortgage insurance, or a structure that does not match your goals.

For a cleaner comparison, ask each company to quote the same loan amount, same down payment, same occupancy type, same credit profile, and same rate-lock period. Then compare the Loan Estimates side by side.

Red flags that deserve a full stop

Some red flags are more than normal sales pressure. If you see one of these, stop and verify before moving forward:

- You are told the rate is guaranteed before your credit, property, income, and loan terms are reviewed.

- You are asked to pay money upfront for mortgage relief or a guaranteed modification.

- You are told to stop communicating with your current lender or servicer.

- You are pushed to transfer the deed to your home.

- You are told to send money by wire, cashier's check, gift card, crypto, or payment app.

- The company name does not match the licensing record, email domain, or documents.

- You are rushed to upload documents through a link you cannot independently verify.

The FTC's mortgage-relief guidance is blunt about this category: scammers often pressure homeowners with promises of help, then demand payment before producing results. If you are in distress, contact your mortgage servicer directly and consider legitimate housing counseling resources before paying anyone who contacted you unexpectedly.

What to do if the offer came from Ratespedia or a partner

Ratespedia's job is to help borrowers find a clearer path through mortgage options. That only works when the borrower knows who they are dealing with and what the next step means.

If an offer or contact came through Ratespedia, slow down and confirm these details:

Should you give your Social Security number to compare mortgage rates?

Sometimes, yes, but not blindly. A lender or broker may need your Social Security number and permission to pull credit to give a more accurate mortgage quote. That does not mean every form deserves that information immediately.

Before entering it, confirm the company, the purpose of the request, the consent language, and whether the next step is a soft inquiry, hard inquiry, prequalification, or full application. If the explanation is unclear, ask for clarification in writing.

Is a very low mortgage rate always a scam?

No. A low rate can be real, especially when a borrower has strong credit, a larger down payment, a lower debt-to-income ratio, or pays discount points. The warning sign is not the low number by itself. The warning sign is a low number without the terms needed to evaluate it.

Ask what the APR is, how many points are included, whether the rate is locked, what the lock period is, what fees apply, and what assumptions were used. A legitimate offer should survive those questions.

How do you know if a mortgage company is licensed?

Start with NMLS Consumer Access. Search the company name, individual name, or NMLS number. Review whether the company information, trade names, branch information, and license status match what you were told.

If the company is a bank, credit union, or other institution with a different regulatory structure, ask the representative how to verify their registration or licensing. A legitimate professional should expect that question.

What should you do if you already shared information?

First, write down what you shared, when you shared it, who received it, and which site, email, phone number, or upload link you used. Then verify the company through official channels.

If you believe you sent money or sensitive information to a scammer, consider reporting it to the FTC at ReportFraud.ftc.gov and reviewing your credit-monitoring or fraud-alert options. If a bank account, wire, or payment app was involved, contact the financial institution quickly.

Do not ignore the feeling that something is off. In mortgage shopping, a short pause to verify the company can protect your identity, money, and homebuying timeline.

The bottom line

You do not need to become a mortgage expert to protect yourself. You need a repeatable process: identify the company, verify the licensing, compare the Loan Estimate, and keep records.

A trustworthy mortgage partner will not be offended by verification. They will help you do it.

Compare mortgage options without guessing

Start with a clear application path and ask questions before sharing documents.

Ratespedia LLC is a licensed mortgage broker. NMLS# 2796610. This article is educational and is not legal, credit, or financial advice. Verify licensing through official regulator resources and review your Loan Estimate before making a mortgage decision.

Written by

Chad Harter

CEO, Ratespedia | NMLS# 2796610

Chad Harter is the founder and CEO of Ratespedia, a licensed mortgage brokerage helping borrowers across the United States find competitive rates and understand their options. With over a decade of experience in mortgage lending and financial services, Chad built Ratespedia to bring transparency and simplicity to one of the most important financial decisions people make. He writes on mortgage markets, personal finance, and borrower strategy.