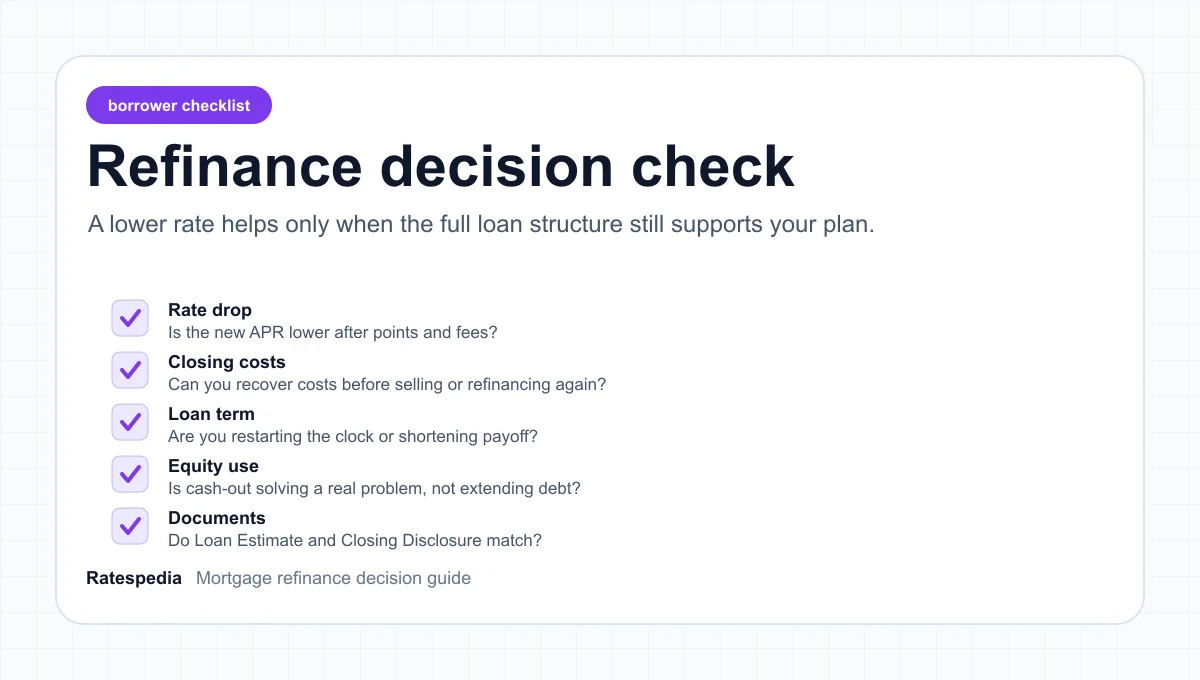

If your current mortgage rate starts with a 7, refinancing deserves a look in 2026. If your current rate starts with a 3 or 4, the answer is probably different. The useful question is not whether refinance rates are "good." The useful question is whether a new loan improves your actual position after closing costs, term reset, mortgage insurance, and the time you plan to keep the home.

As of June 11, 2026, Freddie Mac's Primary Mortgage Market Survey showed the 30-year fixed-rate mortgage averaging 6.52% and the 15-year fixed-rate mortgage averaging 5.84%. That is lower than the 30-year average from a year earlier, but not low enough to make every homeowner a refinance candidate.

Key Takeaways

- Start with break-even math: refinance costs divided by true monthly savings.

- A 0.50% rate drop can help on a large loan, but a 1.00% drop is a cleaner trigger for many borrowers.

- Fannie Mae's June 2026 forecast expects refinance originations to rise sharply from 2025, which means more homeowners are likely to shop.

- Compare APR, points, closing costs, cash to close, and term length, not just the headline rate.

- Cash-out refinancing is different from rate-and-term refinancing because it increases debt secured by your home.

- Ask for a Loan Estimate and review the Closing Disclosure before closing.

The short answer: refinance when the savings survive the costs

Refinancing makes sense when the new loan solves a specific problem and the numbers hold up after costs. That problem might be a lower monthly payment, a shorter payoff timeline, getting out of an adjustable rate, removing mortgage insurance, replacing a high-rate loan, or using equity for a planned purpose.

It does not make sense just because rates moved down for a week. A lower rate can still be a bad deal if the closing costs are high, if the new term stretches the debt too far, or if you plan to sell before you recover the cost.

The refinance decision is not a rate prediction. It is a break-even decision with a time limit.

For a simple first pass, use this formula:

Break-even months = total refinance costs / true monthly savings

If the refinance costs $6,000 and lowers your true monthly payment by $250, the break-even point is 24 months. If you expect to keep the loan for at least three to five years, that might be worth comparing. If you may sell next spring, it probably is not.

What changed in the 2026 refinance market

The 2026 refinance market is more active than the frozen market many borrowers saw after rates rose in 2022 and 2023. That does not mean rates are low. It means more homeowners have loans that are high enough for a refinance quote to be worth testing.

Fannie Mae's June 2026 housing forecast estimated refinance originations of $573 billion in 2025 and $892 billion in 2026. The same forecast showed refinance share rising from 29% in 2025 to 38% in 2026. That is a useful signal: refinance activity is expected to be meaningfully larger, but still very rate-sensitive.

Weekly application data also shows borrowers are responding quickly when rates move. Fannie Mae's weekly mortgage applications data reported that for the week ending June 5, 2026, refinance application dollar volume increased 32.5% from the prior week.

The practical takeaway is simple: when rates dip, refinance windows can get crowded. If you have a high-rate mortgage, it helps to know your target rate, expected savings, documentation needs, and break-even point before you rush into the first quote.

The 1% rule is useful, but incomplete

You have probably heard that refinancing is worth it only if your new rate is at least 1 percentage point lower than your current rate. That rule is helpful because it keeps borrowers from chasing tiny moves. But it is too blunt to use by itself.

A 0.50% rate drop can be worth it if your loan balance is large, closing costs are low, and you plan to keep the mortgage for years. A 1.00% drop can be unattractive if the lender is charging heavy points, if you are resetting from 22 years remaining to a brand-new 30-year term, or if you will move soon.

Use the rate drop as a filter, then run the full comparison.

6.52%

38%

24 mo

Here is the cleaner way to think about it:

| Current rate | New rate | First reaction | What to check next |

|---|---|---|---|

| 7.50% | 6.50% | Strong candidate | Costs, points, term, credit, break-even |

| 7.00% | 6.50% | Maybe | Loan size and how long you will keep the home |

| 6.75% | 6.50% | Usually weak | Only works with very low costs or a larger balance |

| 4.00% | 6.50% | Usually no | Consider home equity options instead of replacing the first mortgage |

If your existing mortgage is far below market, refinancing the whole loan just to access cash can be expensive. In that case, compare a cash-out refinance against a second mortgage option. The Ratespedia guide to home equity loans vs. HELOCs is a better starting point if your main goal is borrowing against equity while preserving a low first-mortgage rate.

Calculate true monthly savings, not just principal and interest

Many borrowers make the refinance decision too quickly because they compare only the principal and interest payment. That can be misleading.

Your true comparison should include:

The CFPB Loan Estimate explainer is useful because it shows where to review closing costs, estimated cash to close, rate lock status, prepayment penalty, balloon payment risk, and mortgage insurance. Do not rely on a verbal quote if you are making a real decision.

For a borrower who only needs lower monthly cash flow, restarting a 30-year term may be acceptable. For a borrower who wants to build equity faster, it may be the wrong move even if the payment drops.

Watch the loan term reset

Term reset is one of the quietest refinance costs. It does not show up as a line item, but it can change the economics of the loan.

Suppose you are 7 years into a 30-year mortgage. You have 23 years remaining. If you refinance into a new 30-year mortgage, you may lower the payment, but you are also adding years back to the payoff schedule. That may be fine if the payment relief is the main goal. It is not fine if your goal is to minimize lifetime interest.

There are three ways to manage that risk:

- Ask for a shorter term, such as a 20-year or 15-year refinance.

- Refinance into a 30-year loan, but keep paying the old payment if your budget allows it.

- Compare total interest over the time you realistically expect to keep the loan, not only over the full 30 years.

The Ratespedia mortgage rate guide is useful here because the same borrower profile that improves a purchase rate can also improve refinance pricing: credit score, debt-to-income ratio, equity, documentation strength, and lender comparison.

When a refinance is likely worth shopping

There is no universal trigger, but these are strong reasons to get quotes:

When waiting is smarter

Waiting can be the right move even when rates are lower than your current loan. The most common reason is a weak break-even window.

If you plan to sell in 12 to 18 months and your refinance breaks even in 30 months, the math is telling you to wait. If the new loan requires heavy discount points to reach an attractive rate, waiting may also be better. Points can make sense when you keep the loan for a long time, but they are expensive if you refinance again soon.

Waiting may also make sense if your credit profile is close to improving. A small credit score gain, lower credit card balance, better debt-to-income ratio, or more home equity can change pricing. If you are near a pricing threshold, ask your loan professional whether a short delay could improve the quote.

Be careful with "no-closing-cost" offers. They can be useful if you do not want to pay cash at closing, but the cost usually appears somewhere else, often as a higher rate or a lender credit that trades long-term interest for short-term convenience. HUD makes a similar point for FHA streamline refinances: "no cost" often means no out-of-pocket expense, not no cost at all.

Rate-and-term refinance vs. cash-out refinance

A rate-and-term refinance replaces your existing mortgage primarily to improve the rate, term, or loan structure. A cash-out refinance replaces the mortgage and increases the loan balance so you receive cash at closing.

Those are different decisions.

Rate-and-term refinance questions:

- How much does the payment fall?

- What is the break-even point?

- Does the new term improve or weaken the payoff plan?

- Are you paying points, and how long until those points pay off?

Cash-out refinance questions:

- How much new debt are you adding?

- Are you replacing a low first-mortgage rate with a higher rate on the full balance?

- Is the cash being used for a high-return purpose, such as necessary repairs or expensive debt payoff?

- Would a home equity loan or HELOC be cleaner?

If you are using equity for a renovation, debt consolidation, or emergency reserve, compare the refinance against the options in Home equity loans vs. HELOCs. Replacing your entire first mortgage is not always the cheapest way to borrow.

FHA streamline refinance: easier does not mean free

If you already have an FHA-insured mortgage, an FHA streamline refinance may be worth checking. HUD explains that streamline refinance means limited borrower credit documentation and underwriting. It does not mean there are no costs.

HUD lists several basic requirements: the mortgage must already be FHA insured, it must be current, the refinance must result in a net tangible benefit, and cash out is limited to no more than $500 in excess proceeds. HUD also notes that FHA does not allow lenders to include closing costs in the new mortgage amount for a streamline refinance.

That makes the offer structure important. A lender may advertise a "no out-of-pocket" streamline by using a higher rate and lender-paid closing costs. That may still be useful, but compare the payment, APR, and break-even logic the same way you would with any other refinance.

What documents should you compare before closing?

Start with the Loan Estimate. Then compare it against the Closing Disclosure before you sign.

The CFPB says the Closing Disclosure must be provided three business days before scheduled closing. Use that time to confirm the final interest rate, monthly payment, loan amount, cash to close, closing costs, prepayment penalty status, and whether anything changed from the Loan Estimate.

If the final numbers are materially different from what you expected, ask why before closing. A refinance should not feel like a surprise at the finish line.

A practical refinance checklist for 2026

Before you apply, write down your target. That keeps the process from turning into rate shopping without a decision rule.

You can also use Ratespedia's mortgage calculators and resources to test payment scenarios before talking through loan options. If you want to confirm Ratespedia licensing, start with the license page.

The bottom line

Refinancing in 2026 is not automatically good or bad. It is borrower-specific. The market is active enough that many homeowners should check the numbers, especially if their current rate is well above current averages. But the best refinance is not the one with the lowest advertised rate. It is the one that improves your payment, term, risk, and total cost within the time you expect to keep the loan.

Start with break-even math. Then pressure-test the term, fees, mortgage insurance, and cash-out tradeoffs. If the savings survive that review, it is worth comparing real offers.

Compare refinance options with a clear target

Start with your current loan details and compare refinance offers against your break-even window.

Ratespedia LLC is a licensed mortgage broker. NMLS# 2796610. This article is educational and is not legal, credit, tax, or financial advice. Rates, forecasts, loan programs, and underwriting requirements change. Review your Loan Estimate and Closing Disclosure before making a mortgage decision.

Written by

Chad Harter

CEO, Ratespedia | NMLS# 2796610

Chad Harter is the founder and CEO of Ratespedia, a licensed mortgage brokerage helping borrowers across the United States find competitive rates and understand their options. With over a decade of experience in mortgage lending and financial services, Chad built Ratespedia to bring transparency and simplicity to one of the most important financial decisions people make. He writes on mortgage markets, personal finance, and borrower strategy.