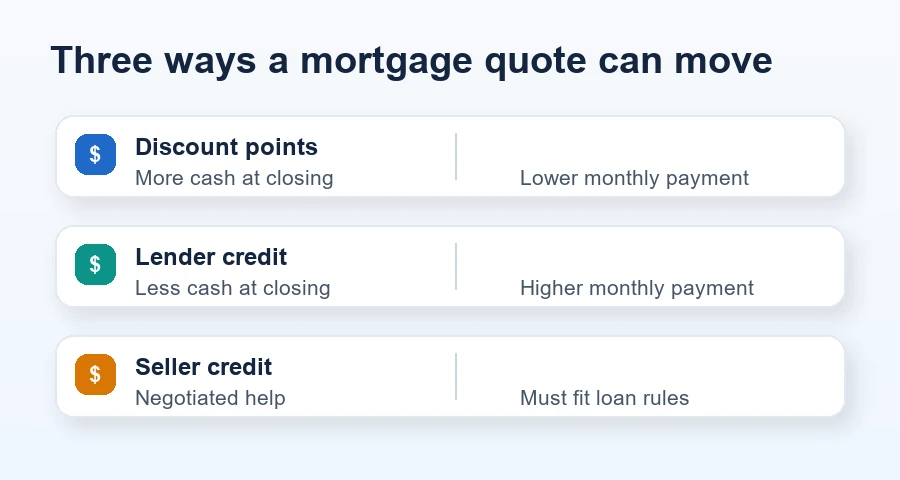

If you are buying a home in 2026, the rate quote is only one part of the deal. The bigger question is how the loan is being priced. A lower rate can come from discount points you pay at closing, a seller credit applied toward closing costs, or a temporary buydown that lowers the payment for the first year or two.

Those options are useful, but they are not interchangeable. Points are usually a long-term bet. Lender credits solve a cash-to-close problem by accepting a higher rate. Seller credits can be powerful, but they must fit program rules and actual closing costs.

As of June 18, 2026, Freddie Mac's Primary Mortgage Market Survey showed the 30-year fixed-rate mortgage averaging 6.47% and the 15-year fixed-rate mortgage averaging 5.81%. The Federal Reserve also held the federal funds rate target range at 3.50% to 3.75% on June 17, 2026, while saying inflation remained above its 2% goal. That is the kind of market where borrowers naturally ask, "Should I buy down the rate?"

Key Takeaways

- Mortgage points lower the rate by increasing upfront closing costs.

- Lender credits lower cash to close by accepting a higher rate.

- Seller credits can help cover points, buydowns, and closing costs, but they have program limits.

- The right answer depends on how long you will keep the loan, not just the monthly payment.

- Compare offers with the same point level, the same loan amount, and the same lock period.

- If you may refinance or sell soon, a large permanent buydown can fail the break-even test.

The short answer: points need time to pay off

Mortgage points are worth considering when you have enough cash after closing, you expect to keep the loan past the break-even period, and the lower rate meaningfully reduces your payment. If any of those pieces is missing, points can make the quote look better without making the loan better.

The basic formula is simple:

Break-even months = upfront point cost / monthly payment savings

If one point costs $4,000 and lowers your payment by $95 per month, the break-even point is about 42 months. That is not automatically good or bad. It depends on whether you realistically expect to keep that mortgage for more than three and a half years.

A lower mortgage rate is not automatically a cheaper mortgage. It depends on what you paid to get that rate and how long you keep it.

This is why a points decision should come after a timeline decision. If you might move, refinance, or sell within two years, paying thousands for a permanent rate reduction may not have enough time to work. If you expect to keep the loan for seven to ten years, the same buydown may be more attractive.

What mortgage points actually buy

Discount points are upfront fees paid to reduce the interest rate. The CFPB explains that one point equals 1% of the loan amount. On a $400,000 mortgage, one point is $4,000. On a $250,000 mortgage, one point is $2,500.

The part borrowers often miss is that one point does not always buy the same rate reduction. The CFPB's discount-points research warns that points have no fixed value in terms of the rate change. One lender might quote a 0.25 percentage point reduction for one point. Another might price the same point differently.

That means you should not compare a 6.25% quote with one point against a 6.50% quote with zero points and assume the lower rate is better. You need to compare the cash, monthly payment, APR, and time horizon together.

6.47%

1%

42 mo

Use the points quote as a pricing question:

| Loan option | Upfront cost | Monthly payment | Best fit |

|---|---|---|---|

| Pay points | Higher cash to close | Lower payment | Longer hold period |

| Zero-point loan | Middle ground | Middle ground | Uncertain timeline |

| Take lender credit | Lower cash to close | Higher payment | Cash preservation |

The zero-point loan is often the clean comparison anchor. Ask for that first, then ask what the payment looks like with points and with a lender credit.

Lender credits are points in reverse

A lender credit does the opposite of a discount point. You accept a higher interest rate, and the lender gives you a credit toward closing costs. The CFPB says lender credits lower what you pay at closing, but the higher rate costs more over time.

That can be the right trade if cash is tight. A borrower with strong income but limited cash after down payment might prefer a slightly higher rate if it keeps the emergency fund intact.

The tradeoff becomes weaker when the credit is small and the rate increase is large. For example, do not accept a meaningfully higher rate for a small credit just because the closing disclosure looks cleaner. Ask how long it takes for the higher monthly payment to exceed the upfront credit.

The Ratespedia guide on how to get the lowest mortgage rate is a useful companion because borrower profile still matters. Credit score, down payment, property type, occupancy, loan size, and debt-to-income ratio can move the base rate before points or credits enter the conversation.

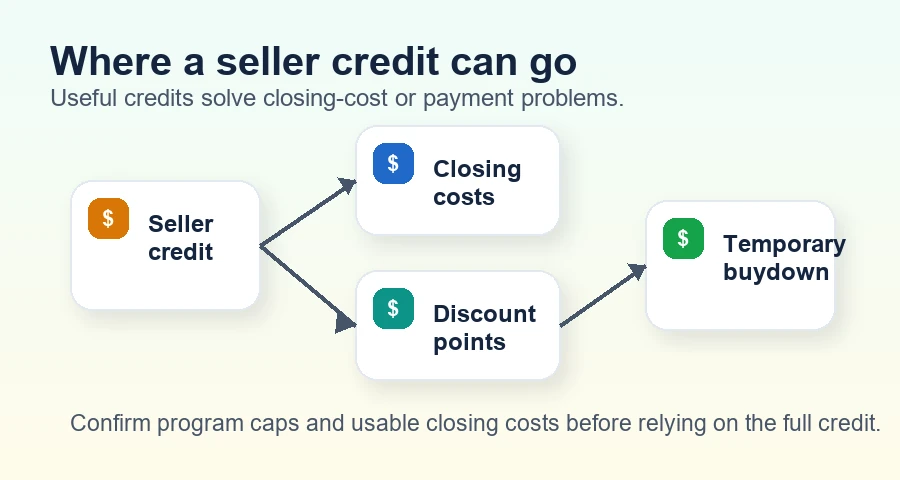

Seller credits can fund the strategy, but they are not free money

Seller credits are negotiated concessions that help cover buyer closing costs. In a market with more inventory or a property that has been sitting, a seller credit can be more useful than a small price reduction because it reduces the cash needed to close.

The latest NAR existing-home sales report for May 2026 showed total housing inventory at 1.55 million units, equal to 4.5 months of supply. That does not mean every buyer has leverage. It does mean buyers in some local markets may have room to ask for credits, especially when a seller wants a cleaner contract rather than another price cut.

Seller credits can often be applied toward closing costs, prepaid items, discount points, or certain buydown structures, depending on loan program rules. They generally cannot be treated as cash back beyond allowable costs. If the credit is larger than eligible closing costs, the excess may be wasted or may create underwriting issues.

Fannie Mae's interested party contribution rules set conventional financing concession limits by occupancy and loan-to-value. For a principal residence or second home, the maximum is 3% when the LTV is greater than 90%, 6% when the LTV is 75.01% to 90%, and 9% when the LTV is 75% or less. Investment properties are limited to 2%.

Permanent buydown vs. temporary buydown

There are two common ways borrowers use the word "buydown."

A permanent buydown usually means paying discount points for a lower interest rate over the life of the loan. The benefit continues as long as you keep that mortgage.

A temporary buydown lowers the borrower's payment for an introductory period while the note rate remains higher. A common example is a 2-1 buydown, where the payment is calculated at a rate 2 percentage points lower in year one, 1 percentage point lower in year two, and then at the full note rate afterward. The subsidy is usually funded by the seller, builder, or another permitted party.

Temporary buydowns can help with payment shock, especially if a buyer expects income growth or wants breathing room after moving. They can also be risky if the borrower only qualifies emotionally at the reduced first-year payment. You need to be comfortable with the full note-rate payment before you close.

Here is the clean distinction:

| Strategy | Helps most with | Main risk |

|---|---|---|

| Permanent points | Long-term interest cost | You move or refinance before break-even |

| Temporary buydown | Early payment relief | Full payment arrives later |

| Lender credit | Cash to close | Higher payment lasts until payoff or refinance |

| Seller credit | Negotiated closing-cost help | Program caps and unused credit |

If you are choosing between a permanent buydown and waiting to refinance later, read Should you refinance your mortgage in 2026?. The same break-even logic applies, but the timing is different: purchase points are paid before you know how long you will keep the loan, while refinance costs are paid after you already own the home.

How to compare offers without getting fooled

Mortgage pricing is easiest to compare when each lender uses the same format. Otherwise, one lender may show a lower rate with points, another may show a higher rate with credits, and a third may quote a temporary buydown that looks cheaper in year one but not afterward.

Ask each lender for three versions:

Then calculate the break-even window for each trade. If the lender credit saves $3,000 at closing but raises the payment by $85 per month, the cost catches up after about 35 months. If you expect to refinance or sell before then, the credit may be attractive. If you expect to keep the loan for seven years, it may be expensive.

The CFPB Loan Estimate guide can help you find the key numbers. Look at the interest rate, APR, projected payments, costs at closing, lender credits, and whether points are included. Do not rely on a screenshot or verbal quote when you are making a binding decision.

When paying points can make sense in 2026

Paying points can make sense when several conditions line up.

Fannie Mae's June 2026 housing forecast projected the 30-year fixed-rate mortgage averaging 6.3% for 2026 and 2027, with forecasts based on rates as of May 29, 2026. Forecasts are not promises, but they are a reminder that no one knows exactly when a better refinance window will arrive.

If you are buying with a low down payment, also compare how points interact with mortgage insurance. The Ratespedia guide to FHA vs. conventional loans can help you think through down payment, mortgage insurance, and program fit before optimizing the rate quote.

When a seller credit is better than a price cut

A seller credit can sometimes help more than a lower purchase price because it reduces the cash barrier at closing. The monthly payment difference from a small price cut may be modest, while a credit can cover closing costs or fund a buydown.

For example, a $10,000 price reduction on a 30-year mortgage may lower the monthly principal-and-interest payment by less than many buyers expect. A $10,000 seller credit, if allowed and usable, could cover prepaid taxes and insurance, lender fees, title charges, or discount points.

That does not mean a credit is always better. A lower price can improve equity, appraisal cushion, and loan-to-value. A credit can disappear if it exceeds allowable closing costs. The right request depends on price, cash position, appraisal, and loan program.

Ask for the concession that solves the actual bottleneck. Sometimes that is payment. Sometimes it is cash to close. Sometimes it is price.

If your main goal is to protect cash because you also plan repairs or renovations, compare the mortgage strategy against other borrowing options. Ratespedia's home equity loan vs. HELOC guide is more relevant after you own the home, but it shows why replacing or layering debt should be compared carefully.

Questions to ask before accepting a buydown

Before you accept a points, credits, or buydown structure, ask these questions and get the answers in writing:

If you receive an unusually low advertised rate, verify whether points are included. The Ratespedia article Is this mortgage offer a scam? walks through the verification steps, including NMLS checks and Loan Estimate review. If you want to confirm Ratespedia licensing, start with the license page.

A practical decision framework

Use this order when you compare options:

- Set your maximum comfortable payment at the full note rate.

- Keep enough cash after closing for reserves and moving costs.

- Ask for a zero-point quote from at least two lenders.

- Compare points and credits against that baseline.

- Run break-even math for each option.

- Apply seller credits only where they solve a real constraint.

- Review the Loan Estimate before locking and the Closing Disclosure before signing.

You can use Ratespedia's resources and calculators to pressure-test payment changes before you talk through quotes. The first pass only needs to tell you whether an offer deserves more attention or should be rejected quickly.

The bottom line

Mortgage points, seller credits, lender credits, and temporary buydowns are pricing tools. None is automatically good. None is automatically bad. The right structure depends on your cash position, loan program, seller negotiation, rate outlook, and expected time in the mortgage.

In 2026, above-6% mortgage rates make buydown conversations more common. That does not mean every buyer should pay points. Start with a zero-point quote, calculate the break-even period, confirm concession limits, and decide whether you are solving a monthly-payment problem or a cash-to-close problem.

If the savings survive that review, a buydown can be useful. If the math depends on refinancing soon, selling soon, or stretching to afford the full payment later, keep shopping.

Compare mortgage options before you lock

Use your loan amount, seller credit, and timeline to compare points, credits, and buydown choices.

Ratespedia LLC is a licensed mortgage broker. NMLS# 2796610. This article is educational and is not legal, credit, tax, or financial advice. Rates, forecasts, seller concessions, and loan-program rules change. Review your Loan Estimate and Closing Disclosure before making a mortgage decision.

Written by

Chad Harter

CEO, Ratespedia | NMLS# 2796610

Chad Harter is the founder and CEO of Ratespedia, a licensed mortgage brokerage helping borrowers across the United States find competitive rates and understand their options. With over a decade of experience in mortgage lending and financial services, Chad built Ratespedia to bring transparency and simplicity to one of the most important financial decisions people make. He writes on mortgage markets, personal finance, and borrower strategy.