An assumable mortgage sounds almost too simple: instead of taking a brand-new loan at today's rate, a buyer takes over the seller's existing mortgage, including its remaining balance, payment schedule, and interest rate. In a market where many current owners still have older, lower-rate loans, that can be a real advantage.

But the useful question is not, "Can I assume a mortgage?" The useful question is, "Can I assume this specific loan, qualify for it, cover the equity gap, protect the seller, and still close on time?"

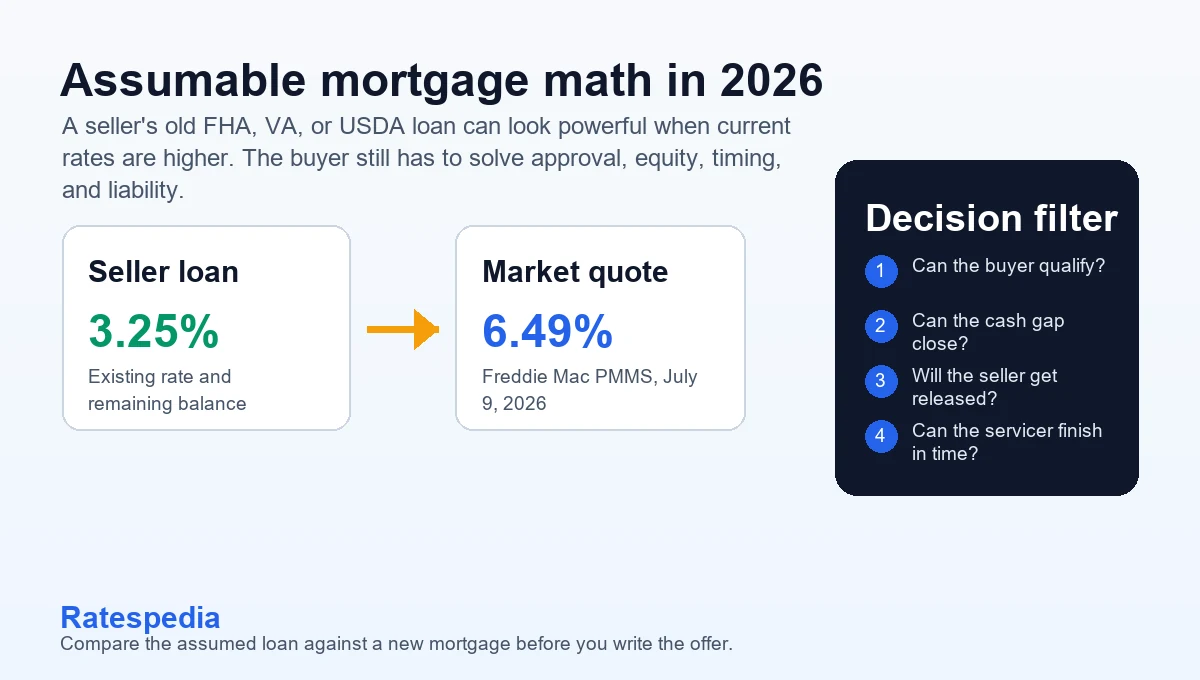

As of July 9, 2026, Freddie Mac's Primary Mortgage Market Survey showed the 30-year fixed-rate mortgage averaging 6.49% and the 15-year fixed-rate mortgage averaging 5.82%. If a seller has an assumable government-backed loan from the low-rate years, the payment difference can be meaningful. The catch is that an assumable loan is not a shortcut around underwriting, cash to close, servicer processing, or contract risk.

Key Takeaways

- FHA, VA, and some USDA loans can be assumable, but most conventional loans are not useful assumption candidates for ordinary buyers.

- The lower rate matters only after you compare the assumed payment, required cash gap, closing costs, mortgage insurance, and second financing.

- The buyer still has to qualify under the applicable program and servicer process.

- VA assumptions need extra seller attention because entitlement and release of liability can follow the loan if handled poorly.

- A seller's low-rate loan may create a large equity gap when the home price is much higher than the remaining loan balance.

- Build a backup plan before writing an offer, because assumptions can move more slowly than a normal purchase loan.

The short answer: an assumable mortgage is worth checking, not chasing blindly

An assumable mortgage is worth checking when the seller's existing loan rate is meaningfully below today's market rate and the remaining loan balance is large enough to matter. It can be especially useful for buyers who find an FHA, VA, or USDA-financed home where the seller still owes a substantial portion of the purchase price.

It is not automatically better than a new loan. If the seller owes far less than the purchase price, the buyer may need a large cash down payment or acceptable second financing. If the servicer process is slow, the contract may need more time. If the buyer cannot qualify, the rate is irrelevant. If the seller does not receive a proper release of liability, the seller may be taking a risk after closing.

The assumed rate is only one part of the deal. The equity gap, approval path, and seller release can decide whether the assumption is actually usable.

For buyers, the best use of an assumption is as one financing path to compare. Run it against a new FHA loan, conventional loan, VA loan, USDA loan, seller credit structure, and any down payment assistance that may be available. The Ratespedia guide to down payment assistance in 2026 is a useful companion because the assumption only solves part of the purchase price.

What is an assumable mortgage?

An assumable mortgage lets a buyer take over the seller's existing mortgage obligation instead of replacing it with an entirely new first mortgage. In plain English, the buyer steps into the remaining loan balance, interest rate, repayment term, and payment structure, subject to approval.

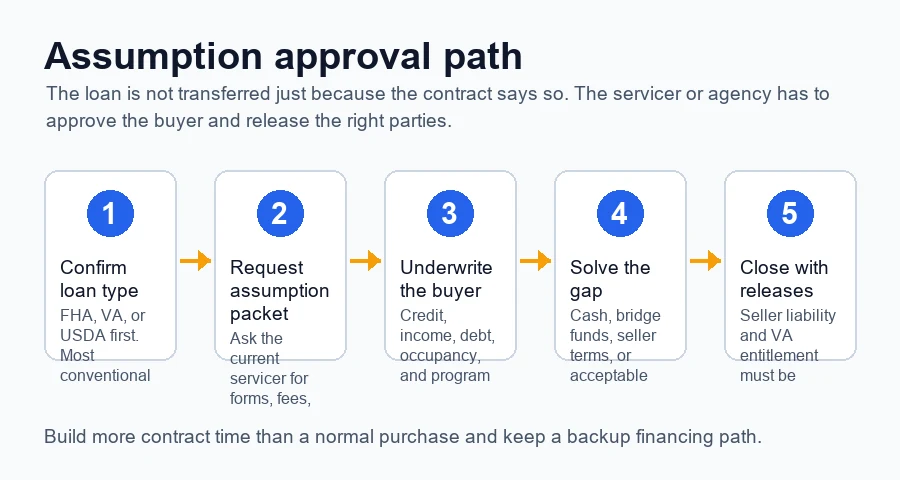

That approval point matters. You do not get the seller's loan just because the purchase contract says "assumption." The loan servicer, lender, agency rules, and closing documents still control the transfer.

The basic structure looks like this:

| Item | What happens in an assumption |

|---|---|

| Existing mortgage balance | Buyer takes over the unpaid balance if approved |

| Interest rate | Buyer may keep the seller's existing note rate |

| Purchase price above balance | Buyer must cover the gap another way |

| Underwriting | Buyer still has to qualify |

| Seller liability | Seller needs a formal release when available |

| Timeline | Servicer and agency processing can add time |

Most buyers hear about assumptions because rates moved up after many sellers locked in lower rates. The CFPB's data spotlight on changing mortgage rates found that nearly 60% of active mortgages had rates below 4% in its dataset, which helps explain why some owners feel locked into their current homes and loans.

That lock-in effect can create an opportunity. A seller who has a low-rate assumable loan may be able to market the home differently. A buyer who can qualify and solve the cash gap may be able to lower the monthly payment compared with a new loan.

Which loans are assumable in 2026?

The practical assumption conversation usually starts with government-backed mortgages: FHA, VA, and USDA. Conventional loans are often written with due-on-sale provisions that make ordinary assumptions unavailable or impractical for a normal purchase.

FHA loans

HUD's assumption guidance says all FHA-insured mortgages are assumable, but newer FHA loans generally require a creditworthiness review. For mortgages closed on or after December 15, 1989, HUD guidance says the borrower who wants to assume the loan must qualify, and the lender or servicer determines creditworthiness under standard mortgage credit analysis.

That means an FHA assumption still has underwriting. The buyer's income, credit, debts, occupancy, source of funds, and secondary financing may all matter. HUD guidance also says the servicer's creditworthiness review should be completed within 45 days after receiving all necessary documents, but the real-world timeline can still depend on how quickly everyone produces a complete package.

FHA assumptions can be attractive when the seller's rate is much lower than today's FHA quote and the buyer fits FHA rules. But FHA mortgage insurance, property condition, and the cash gap still matter. If you are deciding whether FHA is the right foundation, compare the assumption with the Ratespedia guide to FHA vs. conventional loans.

VA loans

VA assumptions can be powerful because a buyer may be able to take over an existing VA-backed loan with a lower rate. VA also makes clear that a non-veteran can assume a VA loan in some cases. But VA assumptions have seller-side consequences that deserve careful attention.

The VA Home Loan Guaranty Buyer's Guide explains that when interest rates rise, assuming a low-rate VA loan could make a home more desirable to a purchaser. It also says the VA funding fee for assumptions is 0.5% unless the buyer is exempt. The same VA guide warns that anyone, even a non-veteran, can assume the loan, but if the buyer is not a veteran substituting entitlement, the seller's entitlement may remain tied to the loan.

VA's Circular 26-23-10 says an assumption must be approved when the loan is current, the assuming buyer is contractually obligated to buy the property and assume full liability, and the buyer is creditworthy under VA standards.

For a VA seller, the key questions are not only price and timing. They are also release of liability and restoration of entitlement. A veteran seller should ask the servicer and VA exactly what happens after closing, especially if the buyer is not using their own VA entitlement.

USDA loans

USDA assumptions are more specialized, but they should not be ignored in eligible rural and smaller-market areas. Federal rules for the USDA guaranteed rural housing program address transfer and assumption of guaranteed loans, including agency approval, buyer eligibility, assumption of the outstanding debt, and transferor liability. That is why USDA assumptions need early servicer and program confirmation instead of assumptions based on the listing alone.

The practical takeaway is that USDA assumptions are not one-size-fits-all. Property eligibility, income eligibility, agency rules, and lender or servicer processing all matter. If the property is in a USDA-eligible area, ask early whether the existing loan is direct or guaranteed, who services it, and what assumption process applies.

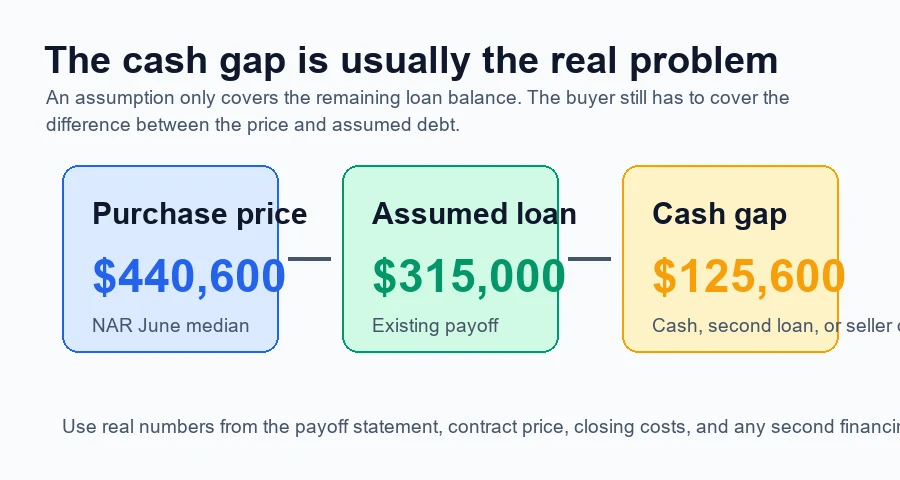

The equity gap is usually the deal breaker

The assumed loan only covers the remaining balance. It does not automatically finance the whole purchase price.

Suppose a seller lists a home for $440,600, which matches the June 2026 median existing-home sales price reported by the National Association of Realtors. If the seller owes $315,000 on an assumable loan, the buyer still has to solve a $125,600 gap before normal closing costs, prepaids, reserves, inspection costs, or any assumption-specific fees.

That gap can be handled in several ways, but each has tradeoffs:

This is where an assumption can stop being a low-rate story and become a cash-to-close story. A buyer may love the assumed rate and still be unable to cover the difference between the home price and the remaining loan balance.

If the gap requires borrowing, compare the payment and risk carefully. The Ratespedia guide to home equity loans vs. HELOCs is written for homeowners, but the same principle applies: layered debt should be compared by payment, rate type, collateral risk, and total cost, not just monthly affordability.

How much can an assumption save?

The savings depend on the existing loan balance, the seller's note rate, today's competing rate, mortgage insurance, loan term, taxes, insurance, fees, and any second financing.

Here is a simple illustration, not a quote:

6.49%

3.25%

0.5%

$1,800

On a $315,000 remaining balance, a 3.25% rate can produce a much lower principal-and-interest payment than a new 6.49% 30-year loan on the same balance. But the buyer does not live on that comparison alone.

The buyer also needs to compare:

- The amount of cash or second financing needed to bridge the purchase price

- Mortgage insurance on the existing loan

- Remaining loan term, not just the rate

- Assumption fees, title fees, escrow setup, taxes, insurance, and prepaid items

- Whether a second loan creates a higher blended payment

- Whether the assumed loan can be refinanced later without creating new problems

If the assumption requires a large second loan at a higher rate, the blended payment may be less attractive than the headline assumed rate suggests. If the buyer has enough cash and the remaining balance is high, the assumption can be much stronger.

Assumption vs. new mortgage: compare the full structure

The right comparison is not "3.25% vs. 6.49%." It is "assumed loan plus cash gap solution" vs. "new loan plus normal down payment and closing costs."

Use this side-by-side framework:

| Question | Assumable mortgage | New mortgage |

|---|---|---|

| What rate applies? | Seller's existing note rate if approved | Current market rate you qualify for |

| How much is financed? | Existing balance only, unless another loan fills the gap | New loan amount based on purchase price and down payment |

| Who underwrites? | Servicer or agency process for assumption | New lender underwriting |

| Biggest risk | Equity gap, timing, release issues | Higher rate, points, mortgage insurance, normal approval risk |

| Best fit | Low seller rate, high remaining balance, buyer has cash or acceptable second financing | Buyer needs simpler financing, higher leverage, or faster closing |

Do not compare the assumed monthly payment to a new-loan payment on the full purchase price without accounting for the cash gap. That makes the assumption look better than it is. At the same time, do not dismiss the assumption just because it is unfamiliar. In the right case, it can be a legitimate payment advantage.

The Ratespedia guide on mortgage points vs. seller credits is useful here because sellers sometimes think a credit or buydown can mimic the assumed rate. It may help, but a temporary buydown, permanent points, seller concession, and true assumption are different tools.

What buyers should ask before writing an offer

Before you build an offer around an assumption, get the facts in writing. A listing description is not enough.

Start with these questions:

If the seller or agent cannot answer these questions, slow down. That does not mean the assumption is impossible. It means the contract needs more due diligence before the buyer treats the low rate as real.

What sellers should protect

Sellers often focus on whether an assumable loan will make the home easier to sell. It can. But the seller should also protect themselves.

The first seller issue is release of liability. If the seller remains responsible after transfer, a future missed payment could become a serious problem. FHA guidance discusses formal release processing, and VA guidance puts extra emphasis on assumption approval and buyer liability. Sellers should not rely on informal promises.

The second seller issue is timing. Assumptions can take longer than a clean new-loan purchase, especially when the servicer is slow, the buyer's package is incomplete, or VA entitlement questions need to be resolved. A seller who needs a fast, certain closing may prefer a buyer with simpler financing even if the assumed loan is attractive.

The third seller issue is price. A low-rate loan can be valuable, but the market still determines what buyers can pay. NAR's June 2026 existing-home sales report showed total inventory of 1.56 million units and a 4.6-month supply. That is more breathing room than the tightest pandemic-era market, but it is not a guarantee that every seller has leverage.

If you are a seller with a VA loan, ask specifically about entitlement restoration. A veteran buyer who substitutes entitlement may be different from a non-veteran buyer who assumes the loan. That difference can matter long after closing.

When an assumable mortgage is likely worth pursuing

An assumption is more likely to be worth pursuing when several pieces line up at once.

The seller's rate should be meaningfully below current market rates. The remaining loan balance should be high enough that the lower rate moves the payment. The buyer should have enough cash, assistance, or acceptable secondary financing to handle the equity gap. The buyer should fit the program's credit and income requirements. The seller should be able to receive the needed release. The contract should leave enough time for the servicer process.

In that situation, the assumption can become a legitimate purchase advantage. It may reduce the monthly payment, improve affordability, or help the buyer qualify for a home that would be harder under a new mortgage.

When a normal mortgage is cleaner

A normal mortgage may be cleaner when the seller's loan balance is too low, the seller's rate is not much better than today's rates, the servicer cannot provide clear timing, the buyer needs high-leverage financing, or the seller needs certainty.

It may also be cleaner when the buyer is trying to force the deal with risky second financing. A low assumed rate can lose its advantage if the gap loan is expensive, adjustable, short-term, or difficult to document.

Buyers should also be careful with listings that overmarket the assumption but understate the approval process. If the pitch sounds too easy, verify the lender, documents, and company identity. The Ratespedia guide on mortgage offer scams explains how to use NMLS Consumer Access, Loan Estimates, and basic verification steps before sending sensitive information.

A practical order of operations

If you want to test an assumable mortgage, follow a sequence:

- Confirm the existing loan type and servicer.

- Get the assumed balance, rate, payment, escrow details, mortgage insurance, and remaining term.

- Ask for the servicer's assumption packet and written timeline.

- Build the buyer's full cash-to-close estimate, including the equity gap.

- Compare the assumption against a new mortgage quote using the same purchase price.

- Confirm release of liability, and for VA loans, entitlement treatment.

- Write the offer with enough time and a backup financing plan.

Ratespedia's resources and calculators can help you pressure-test payment differences before you decide which path is worth pursuing. If you want to verify Ratespedia's licensing, start with the license page.

Compare the assumption against a real mortgage option

Start with the loan balance, rate, cash gap, and backup financing so the low rate is not the only number in the decision.

Bottom line

Assumable mortgages can be useful in 2026 because the market still contains many older loans with rates below today's averages. For the right buyer and seller, taking over an FHA, VA, or USDA loan can create a lower payment than starting over with a new mortgage.

But the assumed rate is not the whole transaction. The buyer has to qualify. The equity gap has to be solved. The seller needs the right release. VA entitlement may need special handling. The timeline has to work. The assumption has to beat a real new-loan alternative after all costs are included.

Treat the assumption as a financing strategy, not a shortcut. If the numbers survive that review, it may be worth pursuing. If they do not, a standard mortgage with clear approval and cleaner timing may be the better deal.

Ratespedia LLC is a licensed mortgage broker. NMLS# 2796610. This article is educational and is not legal, credit, tax, or financial advice. Mortgage guidelines, rates, assumption rules, servicing requirements, seller liability, entitlement rules, income limits, property eligibility, fees, and program terms can change. Review your Loan Estimate, assumption documents, purchase contract, and closing disclosures before making a mortgage decision.

Written by

Chad Harter

CEO, Ratespedia | NMLS# 2796610

Chad Harter is the founder and CEO of Ratespedia, a licensed mortgage brokerage helping borrowers across the United States find competitive rates and understand their options. With over a decade of experience in mortgage lending and financial services, Chad built Ratespedia to bring transparency and simplicity to one of the most important financial decisions people make. He writes on mortgage markets, personal finance, and borrower strategy.