Buying a home in 2026 is not just a rate problem. It is a cash-to-close problem. You can have stable income, workable credit, and a real desire to buy, then still get stuck because the down payment, closing costs, prepaid taxes, insurance, reserves, and repairs arrive at the same time.

That is why down payment assistance gets so much attention. A grant, forgivable loan, deferred second mortgage, gift, seller credit, or low-down-payment mortgage can move a buyer from "not yet" to "maybe now." But assistance is not one simple bucket of free money. Each program has rules, income limits, property limits, timing requirements, and repayment terms.

As of July 2, 2026, Freddie Mac's Primary Mortgage Market Survey showed the 30-year fixed-rate mortgage averaging 6.43%. In a market where the payment is already stretched, using the right assistance structure can matter as much as chasing a slightly lower rate.

Key Takeaways

- Down payment assistance can reduce cash needed at closing, but it can be a grant, forgivable loan, deferred second lien, repayable second mortgage, or credit.

- Start with the full cash-to-close number, not just the minimum down payment.

- FHA can allow 3.5% down, HomeReady and Home Possible can allow 3% down, and VA or USDA may allow eligible buyers to buy with no down payment.

- Assistance rules often depend on income, county, property type, purchase price, homebuyer education, and whether funds are still available.

- Seller credits and lender credits can help with closing costs, but they do not work the same way as down payment funds.

- Get the assistance approval, lender approval, and property eligibility aligned before writing a tight closing timeline.

The short answer: assistance helps only if it survives underwriting

Down payment assistance is worth checking when your monthly payment is workable but your cash to close is the blocker. It is especially useful for first-time buyers, moderate-income households, veterans, rural buyers, buyers in high-cost markets, and borrowers who have income but have not had years to build savings.

The mistake is assuming assistance automatically fixes affordability. It does not. A lender still has to approve the first mortgage. The assistance agency still has to approve the assistance. The property still has to fit program rules. The closing timeline still has to leave room for reservations, education certificates, inspections, and final approval.

Assistance is not a shortcut around loan approval. It is a second set of rules layered on top of the mortgage.

That is why the first question should not be, "How much can I get?" The first question should be, "What kind of help is it, and what does it require from me later?"

What counts as down payment assistance

Down payment assistance is a broad term. In mortgage approval, the details matter.

Grants are usually the cleanest form because they do not have to be repaid if you meet the program rules. Some grants are non-repayable at closing. Others are only forgiven after you live in the home for a certain number of years.

Forgivable second mortgages are common. The assistance may be recorded as a second lien, then forgiven over time if you stay in the home and meet occupancy rules. If you sell or refinance too early, part or all of the balance may become due.

Deferred-payment second mortgages may not require monthly payments, but they are still debt. The balance can become due when you sell, refinance, pay off the first mortgage, move out, or reach a program deadline.

Repayable second mortgages can help with the upfront hurdle, but they add another payment that must fit your debt-to-income ratio.

Gifts from eligible family members or other permitted donors can help, but lenders require documentation. The money has to be sourced, transferred properly, and accompanied by a gift letter.

Seller credits and lender credits can reduce closing costs, but they usually cannot simply replace required borrower funds in every program. The Ratespedia guide to mortgage points vs. seller credits is useful here because credits, points, and cash to close can change the quote in very different ways.

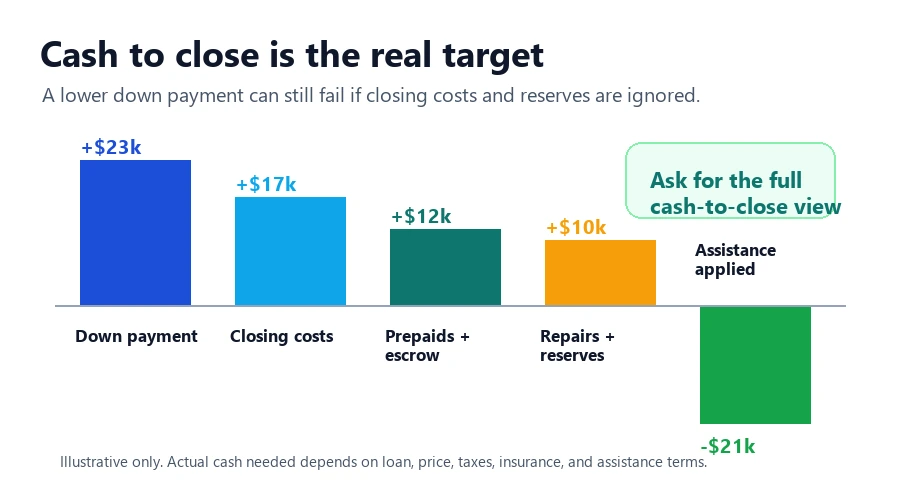

Start with cash to close, not down payment

Many buyers focus only on the down payment because it is the number everyone talks about. But your real closing target is bigger.

Cash to close can include the down payment, lender fees, third-party settlement costs, title and recording fees, appraisal costs, prepaid homeowners insurance, escrow setup, mortgage insurance or funding fees, repairs, inspections, moving costs, and post-closing reserves.

If a buyer says, "I have 3% down," that may still not be enough. On a $350,000 purchase, 3% is $10,500. Closing costs and prepaids can add thousands more. A grant that covers only down payment may not solve cash to close. A seller credit that covers only closing costs may not solve the required minimum investment.

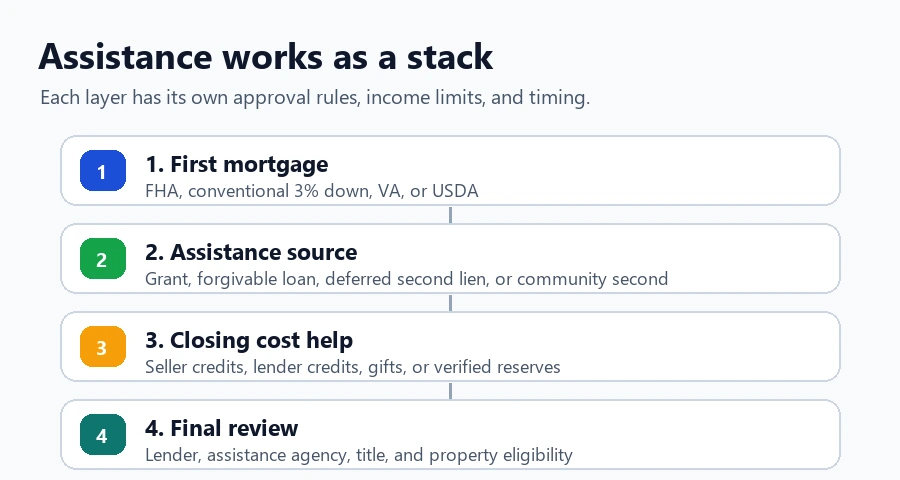

First mortgage programs set the foundation

The assistance layer usually sits on top of a first mortgage. That first mortgage may be FHA, conventional, VA, USDA, or another eligible program. The program affects the minimum down payment, mortgage insurance, property rules, and whether certain assistance sources are allowed.

FHA: common for flexible credit and 3.5% down

HUD explains that FHA loans can allow a down payment as low as 3.5% of the purchase price. FHA is often attractive for buyers with limited savings, lower credit scores, or higher debt-to-income ratios than conventional programs would prefer.

FHA is not automatically cheaper. Mortgage insurance, loan limits, property condition, and seller contribution rules still matter. If you are deciding between FHA and conventional, use the Ratespedia guide to FHA vs. conventional loans before you optimize only around the smallest down payment.

Conventional 3% down: HomeReady and Home Possible

Conventional loans are not only for buyers with 20% down. Fannie Mae's HomeReady underwriting requirements allow up to 97% LTV for one-unit principal residences under Desktop Underwriter, which is the practical 3% down structure many buyers hear about. Freddie Mac's Home Possible mortgage is also a low-down-payment option for qualified low- and very-low-income borrowers.

These programs can be powerful, but they are not open to every borrower in every situation. Income limits, automated underwriting, property type, occupancy, credit profile, and mortgage insurance all matter. If your score is close to a cutoff, read the Ratespedia guide on mortgage credit scores needed to buy a house in 2026 before assuming a 3% conventional loan is available.

VA: zero down for eligible service members and veterans

The VA home loan benefit can be one of the strongest purchase tools in the market. The Department of Veterans Affairs says the VA home loan program does not require a down payment, although lenders can require one in some cases. The VA also notes that VA loans do not require private mortgage insurance.

That does not mean zero cash is always realistic. Buyers still need to consider closing costs, the VA funding fee if applicable, appraisal gaps, repairs, earnest money, and reserves. But for eligible buyers, VA can reduce the biggest upfront barrier.

USDA: no money down in eligible rural areas

USDA's Single Family Housing Guaranteed Loan Program is designed for eligible rural and some suburban buyers. No-down-payment financing may be available for qualified borrowers, but eligibility is local and income-sensitive. USDA's income and property eligibility site is the place to check whether a property location and household income are likely to fit.

USDA is property- and income-sensitive. You need to check whether the property is in an eligible area and whether household income fits the program limit. It can be a strong option, but it is not a general-purpose zero-down loan for every market.

6.43%

3.5%

3%

0% down

State and local assistance can be generous, but specific

The biggest down payment help is often local. State housing finance agencies, cities, counties, employers, nonprofits, and special-purpose programs may offer grants or second mortgages that do not show up in a generic national loan search.

For example, CalHFA's MyHome Assistance Program describes a deferred-payment junior loan of up to the lesser of 3.5% of the purchase price or appraised value for down payment and closing cost help. The Texas Department of Housing and Community Affairs promotes a homebuyer program with flexible down payment assistance and mortgage options. HUD also maintains state and local homeownership assistance pages, such as Florida assistance by county, where buyers can find county-level programs.

Those examples are not a promise that you qualify. They show why the search has to be local. A program may depend on your county, household income, purchase price, occupation, first-time buyer status, veteran status, disability status, or city boundary.

The repayment terms are where many buyers get surprised

Two assistance offers can look identical at closing and behave very differently later.

One program may give you a $12,000 grant that never has to be repaid. Another may give you $12,000 as a silent second mortgage that becomes due when you sell or refinance. A third may forgive 20% per year over five years. A fourth may require monthly payments that count against your debt-to-income ratio.

The repayment rules can affect:

- Whether refinancing later makes sense

- Whether selling in two or three years creates a payoff bill

- Whether you can rent the property later

- Whether the assistance must be repaid if you move out

- Whether a second lien affects future home equity borrowing

This matters in 2026 because many buyers are thinking about refinancing if rates fall later. If assistance creates a second lien, understand whether that lien can be subordinated, forgiven, repaid, or rolled into a future refinance. The Ratespedia guide on whether to refinance your mortgage in 2026 can help you think through that future decision, but the assistance terms should be checked before you close.

Homebuyer education is not a box to ignore

Many assistance programs require homebuyer education or counseling. Treat that as a useful step, not a nuisance.

HUD's housing counseling program helps families obtain, sustain, and retain their homes, and HUD says buyers can find participating counseling agencies through its housing counseling page. The CFPB also provides a tool to find a HUD-approved housing counselor.

Counseling can help you spot questions that do not always appear in a rate quote: what happens if the appraisal comes in low, how much emergency savings should remain after closing, what repairs may be likely in year one, whether the assistance is forgiven or repaid, and whether the program restricts future refinancing.

If you receive an offer that sounds too easy, slow down. The Ratespedia guide on mortgage offer scams explains how to verify companies, Loan Estimates, and NMLS information before you send documents or money. You can also confirm Ratespedia licensing on the license page.

Seller credits can help, but they are not the same thing

Seller credits can be valuable in a slower or more balanced market. The seller agrees to contribute part of the purchase price toward your allowable closing costs. That can reduce the cash you need at closing, but it may not reduce the required down payment unless the loan program allows that specific use.

Seller credits can help pay for closing costs, prepaid taxes and insurance, discount points, temporary buydowns, and certain allowable fees.

They usually cannot cover unlimited costs. Each loan program has interested-party contribution limits. The offer price, appraisal, and market conditions matter too. If you raise the purchase price to get a seller credit, make sure the home still appraises and the payment still makes sense.

This is also where assistance and rate strategy can collide. You might use a seller credit to reduce cash to close, buy down the rate, or offset closing costs. Those are different outcomes. The right move depends on whether your bigger problem is cash, payment, or long-term cost.

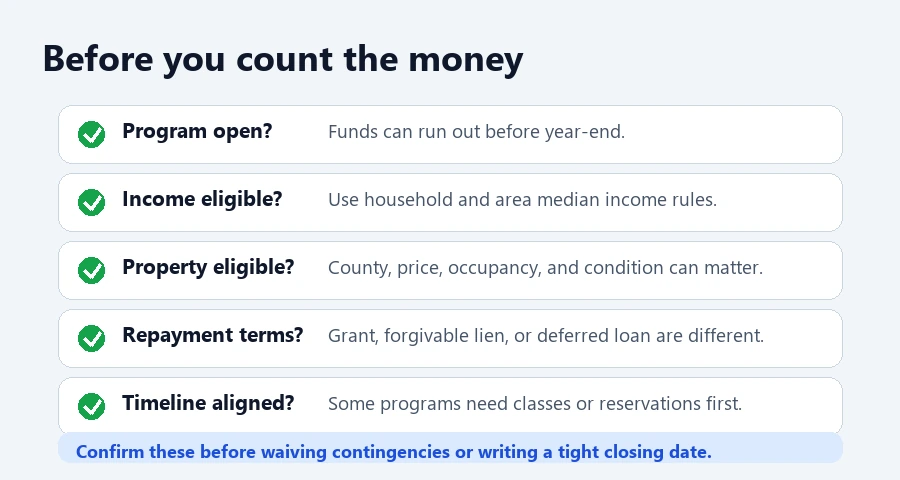

How to compare assistance offers

The cleanest comparison is not the largest dollar amount. It is the assistance that leaves you with a sustainable payment, enough savings after closing, and no repayment surprise later.

Use this checklist before you count an assistance source as real:

A practical order of operations

If you are starting from scratch, do not begin by filling out random grant forms. Build the mortgage file first, then layer assistance around it: estimate your full purchase budget, check your credit and income documentation, compare first-mortgage fit, search local assistance sources, confirm lender participation, ask for a written cash-to-close breakdown, review repayment terms, and write the offer with realistic dates.

Ratespedia's resources and calculators can help you pressure-test payment changes before you talk through options. The goal is not to find the flashiest assistance number. The goal is to find a structure that closes cleanly and still works six months after move-in.

Compare your mortgage options before you shop

Look at loan-program fit, cash to close, assistance options, and payment comfort before you write an offer.

Bottom line

Down payment assistance can be the difference between waiting another year and making a realistic offer in 2026. But the best assistance is the one you can actually close with, understand later, and afford after the keys are yours.

Start with the full cash-to-close estimate. Match the first mortgage to your credit, income, property, and timeline. Then compare assistance by type, not just dollar amount. A smaller grant with clean terms can be better than a larger second lien that creates problems when you sell, refinance, or move.

Ratespedia LLC is a licensed mortgage broker. NMLS# 2796610. This article is educational and is not legal, credit, tax, or financial advice. Mortgage guidelines, rates, assistance availability, lender overlays, income limits, property eligibility, and program terms can change. Review your Loan Estimate, assistance documents, and closing disclosures before making a mortgage decision.

Written by

Chad Harter

CEO, Ratespedia | NMLS# 2796610

Chad Harter is the founder and CEO of Ratespedia, a licensed mortgage brokerage helping borrowers across the United States find competitive rates and understand their options. With over a decade of experience in mortgage lending and financial services, Chad built Ratespedia to bring transparency and simplicity to one of the most important financial decisions people make. He writes on mortgage markets, personal finance, and borrower strategy.