If you are trying to buy a house in 2026, the minimum credit score question has two answers.

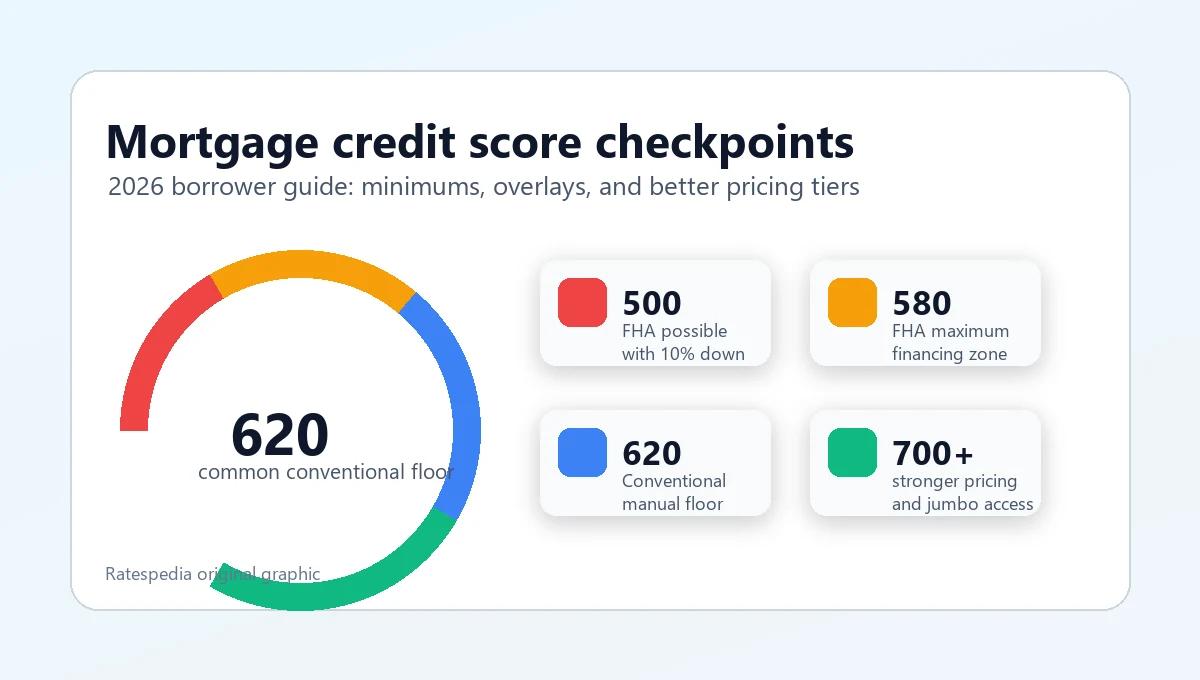

The first answer is the program minimum. FHA can work at 580 with 3.5% down and may go as low as 500 with at least 10% down. Conventional loans commonly start around 620, especially for manually underwritten files. VA and USDA loans are more dependent on lender and automated underwriting results. Jumbo loans usually ask for stronger credit because the loan is outside normal conforming limits.

The second answer is the one that matters for your payment: the score that gets you competitive pricing. In a market where Freddie Mac's Primary Mortgage Market Survey showed the 30-year fixed-rate mortgage averaging 6.47% when checked on June 29, 2026, a thin approval is not the same as a strong offer.

Key Takeaways

- A 620 score is the practical starting point for many conventional mortgage conversations.

- FHA is more flexible: 580 can support 3.5% down, while 500 to 579 generally needs at least 10% down.

- VA does not work like a simple score chart. The lender and automated underwriting result matter.

- USDA eligibility depends on repayment ability, credit history, property location, income limits, and lender/GUS findings.

- Better scores can reduce pricing adjustments, mortgage insurance pressure, and lender-overlay risk.

- Pull your reports before you apply so you can fix errors before a lender prices the loan.

The short answer by loan type

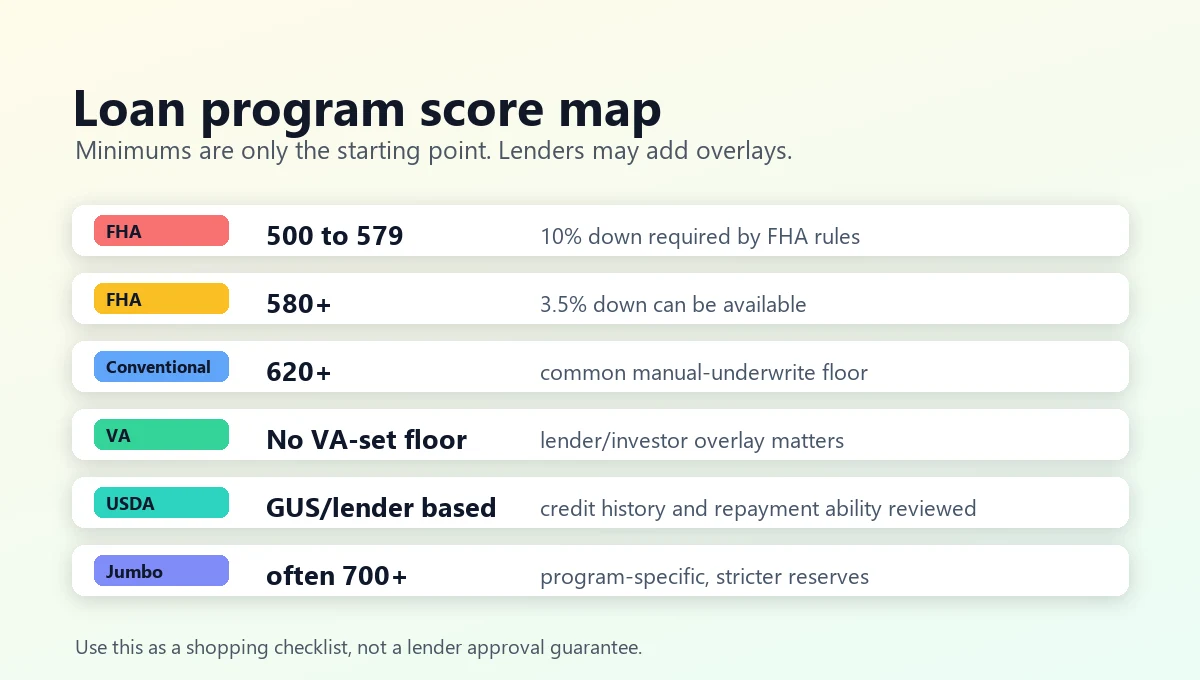

Here is the practical score map most borrowers should use before they apply:

| Loan type | Practical score starting point | What to know |

|---|---|---|

| Conventional | Often 620+ | Stronger scores usually price better, especially with lower down payments. |

| FHA | 580+ for 3.5% down | 500 to 579 may require 10% down and tighter lender overlays. |

| VA | No simple VA-set floor | Many lenders set their own minimums and evaluate the full credit file. |

| USDA | Lender/GUS dependent | Credit history and repayment ability matter as much as the score label. |

| Jumbo | Often 700+ | Large loans usually require stronger credit, reserves, and down payment. |

That table is a starting point, not an approval guarantee. Your actual answer depends on down payment, debt-to-income ratio, reserves, property type, occupancy, loan size, derogatory credit, and the lender's overlays.

If your credit score is right at the edge, do not only ask, "Can I qualify?" Ask, "What does my quote look like if I wait 30 to 60 days and improve the file?" That is often where the savings are.

The minimum score gets you into the conversation. The stronger score helps you control the rate, mortgage insurance, and lender overlays.

Why minimum score and best score are different

Mortgage underwriting is not just a credit-score lookup. A lender is trying to answer three questions:

- Are you eligible for the program?

- Can you repay the loan?

- How should the loan be priced for risk?

The minimum score mostly answers the first question. Pricing answers the third.

Two borrowers can both have a 620 score and receive very different outcomes. One may have a small down payment, high credit-card balances, recent late payments, and limited reserves. The other may have 20% down, low debt, stable income, and one old medical collection. The score is the same, but the file is not.

That is why Ratespedia usually recommends comparing credit, cash, debt, and timeline together. The guide on how to get the lowest mortgage rate is a useful companion because credit is only one rate lever.

6.47%

580

$832,750

Conventional loans: why 620 is only the floor

For a conventional mortgage, 620 is still the score many borrowers hear first. That is a reasonable shorthand, especially for manually underwritten loans and many lender overlays.

The more precise answer is that conventional underwriting depends on the automated underwriting system, the loan characteristics, and the lender's own rules. Fannie Mae's Selling Guide topic B3-5.1-01, updated April 22, 2026, describes how representative credit scores are used and how minimum score rules apply in different underwriting contexts.

For a borrower, the practical lesson is simple: if your middle score is below 620, conventional financing is usually hard. If your score is between 620 and 679, approval may be possible, but pricing and mortgage insurance can be more sensitive. If your score is 700 or higher, more lenders and structures usually become available. If your score is 740, 760, or higher, you are often in a stronger pricing conversation.

Conventional loans also interact with the 2026 conforming loan limit. FHFA announced a baseline one-unit conforming limit of $832,750 for 2026, with a high-cost-area ceiling of $1,249,125. If your loan amount is above the applicable conforming limit, you are usually in jumbo territory, and credit requirements can become stricter.

FHA loans: 580 is the key threshold

FHA is often the first program borrowers consider when credit is bruised or the down payment is small. It is more flexible than many conventional options, but it is not a free pass.

HUD's Single Family Housing Policy Handbook 4000.1 is the FHA source of truth. In plain English, the key FHA score breakpoints are:

- 580 or higher: borrowers may be eligible for maximum financing, commonly discussed as 3.5% down.

- 500 to 579: FHA may still be possible, but the loan-to-value is capped, which generally means at least 10% down.

- Below 500: FHA purchase financing is generally not available.

That does not mean every lender will approve a 580 or 500 score file. Lenders can add overlays. A lender might require a higher score, cleaner recent credit, more reserves, or a stronger debt-to-income ratio than the FHA baseline.

If you are comparing FHA against conventional, read Ratespedia's FHA vs. conventional loan guide. The right answer depends on down payment, mortgage insurance, credit score, loan size, and how long you expect to keep the mortgage.

VA loans: the score is lender-specific

VA loans are different because the Department of Veterans Affairs does not publish the kind of simple minimum-score chart borrowers expect. VA underwriting looks at the overall credit profile, residual income, payment history, and the lender's risk standards.

The VA Lender's Handbook credit underwriting chapter is the better source than internet score charts. It makes clear that VA credit underwriting is a full-file review, not just a one-number rule.

In practice, many VA lenders still use score overlays. A lender may advertise VA options at 620, 600, or another threshold, while a different lender may price or approve the same veteran differently. That is why VA borrowers should compare lenders carefully, especially if the score is below 640 or the debt-to-income ratio is high.

Do not assume a denial from one VA lender means the VA program is unavailable. It may mean that lender's overlay, pricing appetite, or automated underwriting result did not fit your file.

USDA loans: credit history and GUS matter

USDA loans can be attractive because eligible borrowers may buy in approved rural or suburban areas with no down payment. The credit-score answer is less clean than FHA.

The USDA guaranteed-loan regulations in 7 CFR 3555.151 focus on credit qualifications, repayment ability, and underwriting standards rather than a simple public minimum score. In the real world, lenders often talk about 640 because of automated underwriting and investor expectations, but you should verify the lender's current rule before assuming that number is final.

USDA eligibility also depends on household income limits, property location, occupancy, and repayment ability. A 660 score does not help if the property is outside an eligible area or the income calculation does not fit.

Jumbo loans: expect a stronger file

Jumbo loans are not one program. They are mortgages above the applicable conforming loan limit, which means the lender or investor usually keeps more of the risk or sells into a different market.

Because of that, jumbo standards vary more than FHA or conforming conventional loans. Many jumbo lenders want scores around 700 or higher, and some prefer 720, 740, or above for the best pricing. They may also require larger down payments, more reserves, lower debt-to-income ratios, and stricter documentation.

If your credit score is below 700 and the loan amount is near the conforming limit, ask whether changing the down payment, purchase price, or loan structure can bring the first mortgage inside conforming limits. Sometimes the cleanest credit-score strategy is actually a loan-amount strategy.

How credit score changes mortgage pricing

Credit affects pricing in three main ways:

- It can determine whether the automated underwriting system approves the file.

- It can change the interest rate, discount points, or lender credit.

- It can change mortgage insurance cost when the loan has less than 20% down.

A borrower with a 621 score may technically qualify, but the quote can look very different from a borrower at 700, 740, or 760. That difference becomes more visible when rates are already elevated.

If a lender offers a lower rate by charging discount points, make sure you understand the trade. The Ratespedia guide to mortgage points vs. seller credits explains how to compare upfront cost, monthly savings, and break-even time.

Credit score also affects refinance flexibility. If you buy now with a thin approval, improving your credit after closing may help if you refinance later. But refinancing has costs, so do not count on a future refinance to make today's weak structure work. Use the mortgage refinance break-even guide before assuming a later refinance will solve the problem.

What lenders look for besides the score

When a lender reviews your file, these details can matter as much as the score itself:

That is why the strongest mortgage applications are usually boring. Stable income, documented funds, low revolving balances, no recent late payments, and no surprise debts make the underwriter's job easier.

How to improve your mortgage file before applying

The best credit work happens before the lender pulls credit. Once a lender has a tri-merge report and you are under contract, you may have less time to fix problems.

Start with your reports. The CFPB's credit reports and scores guide explains why reviewing your reports matters, and AnnualCreditReport.com is the official site for free reports from the three nationwide credit bureaus.

Use this order:

- Pull all three reports and save the report date.

- Look for wrong balances, duplicate collections, incorrect late payments, and accounts that are not yours.

- Dispute true errors through the bureau and keep documentation.

- Pay down revolving balances before statement closing dates when possible.

- Avoid opening or co-signing new credit.

- Do not finance furniture, appliances, a vehicle, or buy-now-pay-later purchases before closing.

- Keep cash movements simple and documented.

If you receive a surprisingly low advertised mortgage offer while you are shopping, verify the lender and the Loan Estimate. Ratespedia's guide on mortgage offer scams walks through the checks. You can also confirm Ratespedia licensing on the license page.

Should you wait to improve your score?

Waiting can make sense when the score improvement is realistic, the purchase timeline allows it, and the expected pricing benefit is meaningful.

You might wait if:

- Your score is just below 580, 620, 700, 740, or another lender pricing threshold.

- Your credit-card balances are temporarily high but can be paid down quickly.

- A true credit-report error is suppressing your score.

- A recent inquiry or new account is about to age enough to matter.

- You need more reserves or a smaller debt-to-income ratio anyway.

You might not wait if:

- Home inventory is limited and the property is a strong fit.

- Your score issue will take many months to repair.

- The current approval is solid and the payment is comfortable.

- You have enough seller credit or lender credit to solve the cash problem without overpaying long term.

This is where a real comparison helps. Ask the lender to show today's quote and a hypothetical quote at the next realistic score tier. If the difference is small, waiting may not matter. If the difference changes approval, mortgage insurance, or points by a lot, the delay may be worth it.

Questions to ask your lender

Before you accept a preapproval, ask direct questions:

Use Ratespedia's resources and calculators to pressure-test payment changes before you lock. A better score is only useful if the final payment, cash to close, and loan structure fit your budget.

The bottom line

For most 2026 homebuyers, the practical score checkpoints are 580 for FHA maximum financing, 620 for many conventional conversations, and 700 or higher for stronger pricing and jumbo flexibility. VA and USDA are less about a public score chart and more about lender overlays, automated findings, and full-file strength.

Do not stop at the minimum. Ask what score improves the quote, what debt or balance changes could move you there, and whether waiting is worth the tradeoff.

If your file is close, small credit cleanup can matter. If your file is already strong, the better use of time may be comparing lenders, loan structures, seller credits, points, and lock options.

Check your mortgage options before you shop

Compare loan-program fit, credit-score thresholds, and payment comfort before you lock into a rate quote.

Ratespedia LLC is a licensed mortgage broker. NMLS# 2796610. This article is educational and is not legal, credit, tax, or financial advice. Mortgage guidelines, rates, lender overlays, loan limits, and pricing can change. Review your Loan Estimate and program-specific requirements before making a mortgage decision.

Written by

Chad Harter

CEO, Ratespedia | NMLS# 2796610

Chad Harter is the founder and CEO of Ratespedia, a licensed mortgage brokerage helping borrowers across the United States find competitive rates and understand their options. With over a decade of experience in mortgage lending and financial services, Chad built Ratespedia to bring transparency and simplicity to one of the most important financial decisions people make. He writes on mortgage markets, personal finance, and borrower strategy.